Every gas leak is both a regulatory failure and a human risk. The industrial world is finally learning to listen in real time.

ROCKVILLE , MD, UNITED STATES, April 21, 2026 /EINPresswire.com/ — YOUR PLANT IS SPEAKING. Does Your Safety System Know How to Listen? How USD 4.37 Billion in Gas Detection Revenue Is Scaling to USD 7.23 Billion by 2032

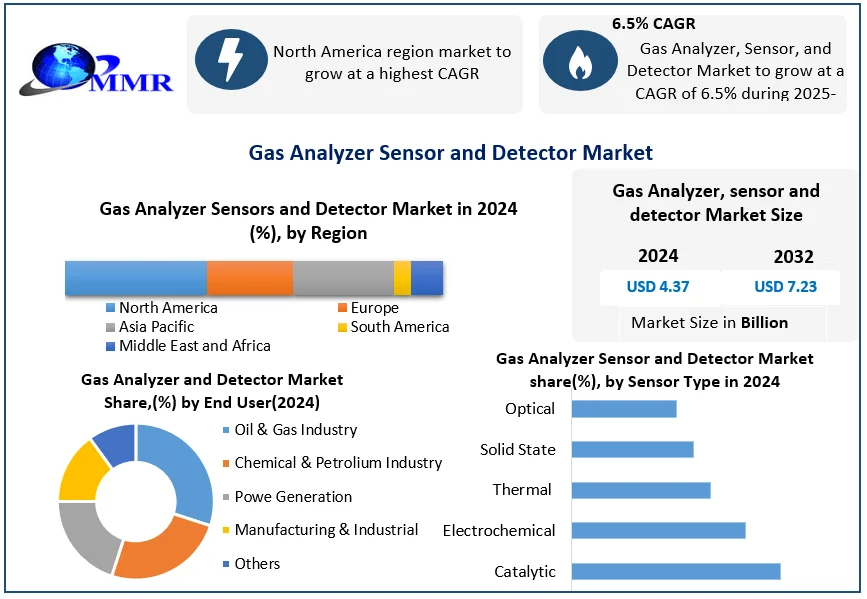

Global Gas Analyzer Sensor and Detector Market was valued at USD 4.37 Billion in 2024 and is projected to reach USD 7.23 Billion by 2032, expanding at a CAGR of 6.5% through the forecast period. Gas analyzers, sensors, and detectors are no longer passive safety instruments; they are the first-line intelligence layer of industrial operations. From subsea oil platforms running methane and hydrogen leak detection protocols to petrochemical refineries deploying continuous emission monitoring systems (CEMS) for EPA ambient air protocol compliance, these devices underpin every regulatory framework that governs industrial production. Honeywell, MSA Safety, Emerson, and Siemens command the market through a combination of NDIR gas detection technology leadership and integrated wireless gas detector ecosystems that convert point measurement into plant-wide operational intelligence.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @ https://www.maximizemarketresearch.com/request-sample/281530/

Safety as Strategic Investment

Three forces are shifting gas detection from a cost center to a strategic asset. First, stringent OSHA/EPA mandates have made monitoring a legal necessity. Second, IoT-integrated sensors provide an 18% reduction in unplanned downtime, offering clear operational ROI. Finally, ESG reporting requires investor-grade data infrastructure. Honeywell’s 2025 platform exemplifies this, cutting leak-response times by 67% and converting safety spending into high-value industrial intelligence.

Barriers to Mid-Tier Adoption

Widespread deployment faces significant cost hurdles. Enterprise-grade portable gas detection solutions range from $800 to $3,500, creating friction for smaller enterprises. Beyond initial procurement, calibration complexity for electrochemical sensors and sensor drift in harsh industrial environments inflate the total cost of ownership. These ongoing maintenance requirements often exceed initial budgets, stalling the transition to advanced wireless monitoring in humidity-heavy or high-temperature facilities.

The $2.86 Billion Growth Corridor

Future demand is concentrated in three high-growth areas. The EU Soil Health Law creates a new category for methane flux measurement. Simultaneously, the hydrogen economy requires specialized catalytic gas sensors for leak detection at electrolysis plants. Lastly, carbon capture (CCS) mandates permanent CEMS at injection wells. The European Commission’s 2025 directive alone adds $380 Million in addressable procurement, locking in regulation-driven demand through 2027.

Which Sensor Type, Gas Category, and End Industry Are Capturing the Largest Revenue Share?

By sensor type, catalytic gas sensors hold 34% market share, valued for reliability and cost-effectiveness in hydrocarbon detection for oil and gas and mining applications. NDIR gas detection technology is the fastest-growing segment, driven by its precision, longevity, and expanding application in continuous emission monitoring systems for CO2 and NOx. By gas type, toxic gas detection commands the largest revenue pool driven by OSHA permit-required confined space regulations. By end-use, Oil and Gas leads with 38% revenue share, followed by mining at 22% and chemicals at 18%.

By Sensor Type

Catalytic Gas Sensors

NDIR Technology Sensors

Electrochemical Gas Sensors

Photoionization Detectors

Others

By Gas Type

Toxic Gas

Combustible and Flammable Gas

Volatile Organic Compounds

Carbon Dioxide and Greenhouse Gases

Others

By End Use

Oil and Gas

Mining

Chemicals and Petrochemicals

Environmental Monitoring

Food and Beverage

Others

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @ https://www.maximizemarketresearch.com/request-sample/281530/

North America Sets the Regulatory Standard. Which Region Is Growing the Fastest and Why?

North America: Dominant Market Leader

North America commands the largest share of Global Gas Detection Revenue, underpinned by OSHA’s Process Safety Management standard, EPA’s Risk Management Plan requirements, and the deepest concentration of oil and gas, chemical, and mining operations globally. Honeywell, MSA Safety, and Industrial Scientific have manufacturing and service infrastructure embedded throughout the region’s refinery and extraction corridors, creating specification-locked procurement relationships.

Asia-Pacific: Fastest-Growing Region

Asia-Pacific is growing at the highest regional CAGR, driven by China’s accelerating industrial safety enforcement, India’s Petroleum and Explosives Safety Organisation (PESO) mandate expansion, and Southeast Asian LNG terminal buildout requiring specialized cryogenic gas detection. Government-mandated safety audits at manufacturing facilities across the region are converting previously unmonitored facilities into active sensor procurement targets.

Four Technology Shifts That Are Making 2020-Era Gas Detectors Commercially Obsolete

Wireless and IoT Integration Transforms Discrete Sensors Into Plant Intelligence Networks

Next-generation wireless gas detectors with mesh networking capability, edge AI processing, and cloud connectivity are converting isolated point sensors into plant-wide safety intelligence networks, enabling facility managers to visualize gas distribution in real time across entire production floors.

NDIR Technology Achieves Sub-PPM Precision at Industrial Scale

Advances in NDIR gas detection technology optics and signal processing have pushed detection limits below 1 ppm for CO2, methane, and nitrogen oxides, enabling hazardous gas emissions monitoring applications that electrochemical sensors cannot match in high-temperature or high-humidity industrial environments.

Portable Multi-Gas Detectors Democratize Advanced Detection

Miniaturization of portable gas detection solutions has produced sub-500g, 4-gas simultaneous detection units at price points now accessible to SME operators, expanding the total addressable market for cost-effective gas analyzers for small enterprises by 40% since 2022.

Hydrogen-Specific Sensors Open a New Market Category

The hydrogen economy’s infrastructure buildout is requiring specialized methane and hydrogen leak detection technology with rapid response times below 30 seconds at 0.1% LEL, creating a sensor specification that existing catalytic and electrochemical technologies cannot meet without redesign, driving next-generation sensor development investment.

Who Holds the Most Defensible Position in the Global Gas Analyzer Sensor and Detector Market?

The Gas Analyzer Sensor and Detector Market is moderately consolidated. Honeywell Analytics leads through sensor technology breadth and global service network depth. MSA Safety and Industrial Scientific dominate the personal protective equipment integration segment where gas detectors are bundled with full PPE ecosystem specifications. Emerson Electric and Siemens command the process analytics and CEMS segment through deep control system integration. New entrants from South Korea and China are challenging mid-tier NDIR and electrochemical segments with 30-40% cost advantages, compressing margins for Western incumbents outside their specification-locked enterprise accounts.

Gas Analyzer Sensor and Detector Market Key Players

North America

1. Honeywell International Inc.: United States

2. Emerson Electric Co.: United States

3. MSA Safety Incorporated: United States

4. GE Analytical Instruments – United States

5. Thermo Fisher Scientific – United States

Europe

1. Draegerwerk AG & Co. KGaA – Germany

2. ABB Ltd. – Switzerland

3. Endress+Hauser – Switzerland

4. Siemens AG – Germany

5. GFG Instrumentation – Germany

Asia Pacific

1. Hangzhou Zetian Technology Co., Ltd. – China

2. Beijing SG Technology Co., Ltd. – China

3. China National Petroleum Corporation (CNPC) – China

4. Metrasens India Pvt Ltd – India

5. Hitech Sensors India Pvt Ltd – India

Get access to the full description of the report @ https://www.maximizemarketresearch.com/market-report/gas-analyzer-sensor-and-detector-market/281530/

Key Recent Developments in the Global Gas Analyzer Sensor and Detector Market

April 2025: Honeywell — AI-Powered Refinery Platform Honeywell launched a connected gas detection platform for refineries featuring AI-based anomaly detection across 200+ sensor nodes. This development reduces leak-to-response time by 67%, setting a new IoT integration benchmark for the industry.

February 2025: Emerson Electric — Hydrogen Economy Unlock Emerson introduced the Rosemount CT4215, the first industrial-grade NDIR gas analyzer optimized for continuous H2 monitoring. This innovation captures an entirely new procurement category within the rapidly expanding hydrogen production sector.

January 2025: European Commission — Regulatory Mandate The finalized Industrial Emissions Directive now requires real-time Continuous Emission Monitoring Systems (CEMS) at 4,200 additional facilities. This mandate adds $380 Million in addressable procurement, forcing large-scale sensor network upgrades across Europe.

October 2024: Siemens — Predictive Compliance Management Siemens expanded its portfolio with AI-powered NOx and CO2 emission prediction. By converting CEMS from reactive measurement to predictive management, Siemens has significantly increased per-unit value and compliance reliability for industrial operators.

FAQs: Global Gas Analyzer Sensor and Detector Market

Q1. What is the Gas Analyzer Sensor and Detector Market Size?

Ans. Valued at $4.37 Billion in 2024, the market is projected to reach $7.23 Billion by 2032 at a 6.9% CAGR, driven by OSHA/EPA compliance and the hydrogen economy.

Q2. Which sensor technology leads?

Ans. Catalytic sensors hold a 34% share for hydrocarbon detection, while NDIR technology is the fastest-growing due to its precision in Continuous Emission Monitoring Systems (CEMS).

Q3. How does the EU Soil Health Law impact demand?

Ans. The law mandates methane and CO2 measurement, creating a new $200M+ category for portable gas analyzers through 2032.

Q4. How is refinery safety driving growth?

Ans. Platforms like Honeywell’s 2025 connected system cut leak-response time by 67%, turning safety spending into strategic operational ROI.

Q5. Which regions lead growth?

Ans. North America leads due to regulatory depth, while Asia-Pacific is the fastest-growing hub, fueled by industrial safety mandates in China and India.

Analyst Perspective

Analysts view the 6.9% CAGR as a regulatory-anchored trajectory, insulated from economic cycles. Demand is secured by OSHA enforcement, EU IED expansion, and hydrogen infrastructure. High-margin growth is concentrated in NDIR technology and wireless IoT detectors that integrate predictive analytics. The 2027 EU mandate represents the largest regulatory demand event in history, providing a robust, non-cyclical procurement foundation through 2032.

Related Reports

Industrial Safety Market: https://www.maximizemarketresearch.com/market-report/industrial-safety-market/3406/

Industrial Safety Market by Product, Application, End-User, and Region, Global Forecast to 2032

Air Quality Monitoring Market: https://www.maximizemarketresearch.com/market-report/air-quality-monitoring-market/15476/

Air Quality Monitoring Market by Product, Pollutant, Application, and Region, Global Forecast to 2032

Environmental Monitoring Market: https://www.maximizemarketresearch.com/market-report/environmental-monitoring-market/3521/

Environmental Monitoring Market by Component, Application, End-User, and Region, Global Forecast to 2032

Industrial IoT Market: https://www.maximizemarketresearch.com/market-report/industrial-internet-of-things-iiot-market/8038/

Industrial IoT Market by Component, Technology, Application, End-User, and Region, Global Forecast to 2032

Emission Monitoring Systems Market: https://www.maximizemarketresearch.com/market-report/continuous-emission-monitoring-systems-market/19944/

Emission Monitoring Systems Market by Component, Type, End-Use Industry, and Region, Global Forecast to 2032

Top Reports:

Automotive Battery Powered Propulsion System Market

Corrosion Inhibiting Additives Market

About Maximize Market Research Pvt. Ltd.

Maximize Market Research is a premier global consulting firm headquartered in Pune, India. Serving clients across 45+ countries, MMR delivers high-granularity market intelligence across Industrial Safety, Chemical and Material, Energy and Power, and Environmental Technology, empowering enterprises with data-driven insights to make strategic decisions with confidence.

Domain Focus

This report falls under Maximize Market Research’s Chemical and Material domain, spanning gas analyzers, industrial sensors, emission monitoring systems, and environmental detection technology across 45+ countries, delivering the intelligence industrial safety managers, regulatory compliance officers, and capital equipment investors need to navigate the evolving global gas detection market through 2032.

Lumawant Godage

MAXIMIZE MARKET RESEARCH PVT. LTD.

+91 96073 65656

akash.r@maximizemarketresearch.com

Visit us on social media:

LinkedIn

Instagram

Facebook

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery