![]()

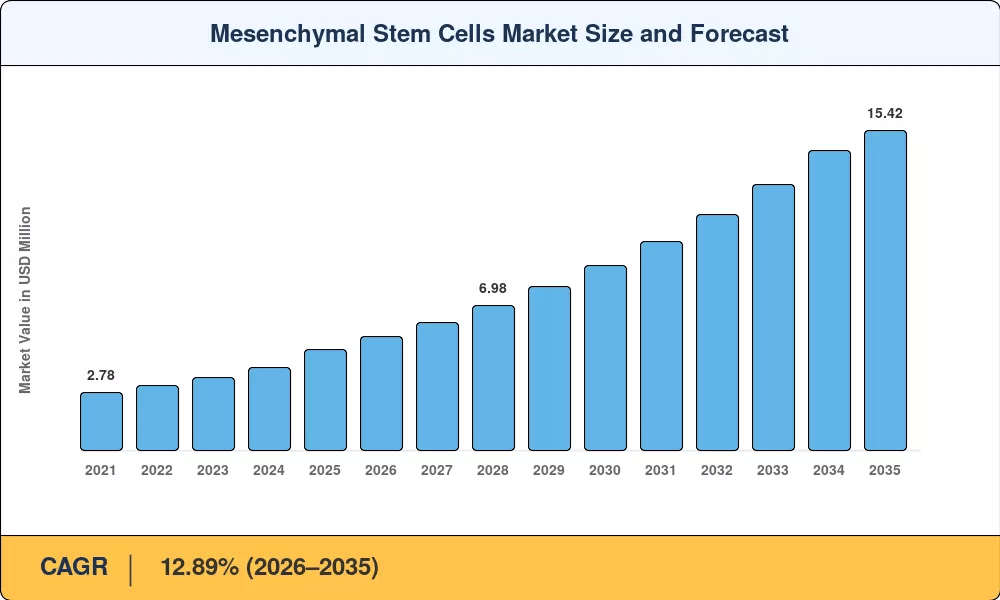

Mesenchymal Stem Cells Market to Surge from USD 5.48 Billion in 2026 to USD 15.42 Billion by 2035—Powered by Landmark Allogeneic MSC Regulatory Clearances

NY, CA, UNITED STATES, June 17, 2026 /EINPresswire.com/ — As per Market Research Future, the global Mesenchymal Stem Cells Market size to reach USD 15.42 Billion by 2035 from USD 5.48 Billion in 2026, at a CAGR of 12.89% during the forecast period 2026–2035. The market base was estimated at USD 4.89 Billion in 2025.

The 12.89% CAGR—anchored by the landmark 2024 regulatory clearance of Ryoncil, the first allogeneic mesenchymal stromal cell product approved in North America—is driven by three converging forces: accelerating regulatory pathway designations (RMAT, SAKIGAKE, PRIME) that have compressed median review timelines by approximately 35%, sustained bioreactor scale-up and closed-system manufacturing investments that have cut batch-failure rates by up to 40%, and expanding reimbursement codes for regenerative cell transplantation that are converting investigational MSC cell therapy applications into billable, standardized care pathways.

National governments and multilateral health organizations are amplifying this momentum. The FDA’s Regenerative Medicine Advanced Therapy (RMAT) designation has cut median review timelines for bone marrow stromal cell products by approximately 35%, according to agency data published in late 2024. Venture capital commitments to regenerative cell transplantation platforms exceeded USD 3.2 billion globally during 2023–2024, signaling that commercial confidence has caught up with the science.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/21855

Key Market Trends & Growth Drivers

Regulatory Pathway Acceleration and Landmark Clearances

The FDA’s Regenerative Medicine Advanced Therapy (RMAT) designation has cut median review timelines for bone marrow stromal cell products by approximately 35%, according to agency data published in late 2024. Japan’s SAKIGAKE fast-track and the EMA’s PRIME scheme mirror this intent, collectively creating a regulatory tailwind that compresses the timeline from pivotal trial to first commercial sale. Ryoncil’s 2024 clearance—achieved in under 18 months from BLA submission—set the benchmark, and at least four additional allogeneic MSC cell therapy applications are now in rolling review across these three jurisdictions.

The landmark 2024 regulatory clearance of Ryoncil—the first allogeneic mesenchymal stromal cell product approved in North America—validated the entire therapeutic class and unlocked institutional reimbursement pathways. South Korea’s MFDS expanded its conditional approval framework in March 2025 to cover three new indications for MSC cell therapy applications, including degenerative disc disease and diabetic foot ulcers.

Bioreactor Scale-Up and Closed-System Manufacturing

Traditional flask-based expansion of mesenchymal stromal cells yields roughly 10⁸ cells per batch; stirred-tank and hollow-fiber bioreactors push output past 10¹⁰ cells while reducing labor costs by 50–60%. Companies like Lonza and Cytiva have invested over USD 800 million combined in dedicated cell therapy manufacturing suites since 2022, directly expanding capacity for multipotent stromal cell research-grade and clinical-grade production. Closed-system processing also mitigates contamination risk, which historically accounted for 12–15% of batch failures in open-system workflows.

Legacy bone marrow aspiration protocols are giving way to closed-system bioprocessing platforms that standardize multipotent stromal cell research outputs and cut batch-failure rates by up to 40%. Companies combining proprietary adipose-derived stem cell lines with automated expansion bioreactors are attracting the largest Series B and C rounds, while diversified pharmaceutical groups are acquiring contract manufacturers to lock in supply resilience for MSC cell therapy applications.

Expanding Reimbursement and Regenerative Cell Transplantation Access

Commercial payers and public health administrators are methodically creating product-specific Healthcare Common Procedure Coding System (HCPCS) codes in response to the FDA’s certification of the first commercial allogeneic MSC treatment framework. While established pathways for approved orphan and critical-need indications are providing the fundamental blueprints for expanded private carrier reimbursement structures, investigational designations continue to limit broad coverage for off-label applications such as osteoarthritis. In the United States, CMS reimbursement codes for regenerative cell transplantation under the hospital outpatient prospective payment system have driven adoption in academic medical centers, while community oncology networks increasingly prescribe MSC cell therapy applications to manage chronic disease burden.

The move from open-system to closed-system bioprocessing—as seen with automated expansion bioreactors—decreases batch-failure rates from 12–15% to under 2%. Hospital cell-processing centers and academic medical centers are seeing a rising preference for standardized allogeneic products due to lower operating costs and higher patient throughput. This efficiency-driven adoption is expected to open up incremental income for the Mesenchymal Stem Cells Market in the absence of patient-specific manufacturing delays.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/21855

Market Segment Insights

BY PRODUCTS & SERVICES

Kits, Media & Reagents: Dominant segment with ~54.8% revenue share in 2025. Reflecting heavy demand for standardized multipotent stromal cell research consumables. Standardized expansion protocols for bone marrow stromal cells anchor institutional procurement globally due to their essential role in every clinical and research workflow. Hospital procurement teams treat culture media, growth factors, and characterization antibodies as default first-line consumables, and the “razors and blades” revenue model has enabled broad adoption even in cost-sensitive emerging markets.

Cells & Cell Lines: Fastest-growing product segment at 14.25% CAGR (2026–2035). Driven by direct clinical-use allogeneic banking and expanding regenerative cell transplantation indications. Mesoblast’s Ryoncil generated landmark revenue in 2024–2025, and pipeline allogeneic MSC candidates targeting cardiovascular and orthopedic indications could double the segment’s addressable population by 2030. The convergence of diagnostic potency analytics with therapeutic cell banking is creating platform economics that personalize regenerative cell transplantation at scale.

BY TYPE

Allogeneic: Dominant type with ~62.5% revenue share in 2025. Benefiting from off-the-shelf logistics and scalable manufacturing for regenerative cell transplantation. Allogeneic therapies lead because they eliminate the patient-specific manufacturing step, cutting time-to-treatment from weeks to hours. Firms that pair master cell banks with validated thaw-and-inject protocols can serve emergency indications such as acute graft-versus-host disease within hours of clinical decision, a logistics advantage that autologous competitors cannot replicate.

Autologous: Fastest-growing type segment at 14.31% CAGR (2026–2035). Driven by personalized MSC cell therapy applications in orthopedic and autoimmune indications. Autologous approaches retain appeal in indications where immune matching is critical and are projected to grow faster as point-of-care adipose-derived stem cells processing devices reach commercial maturity.

BY SOURCE

Bone Marrow: Dominant source with ~36.1% revenue share in 2025. Longest clinical track record and validated potency assays for bone marrow stromal cells anchor institutional formularies globally. Iliac crest aspiration protocols remain the gold standard due to decades of clinical data, and established potency assays have enabled broad adoption even in regulatory-sensitive markets.

Adipose Tissue: Fastest-growing source segment at 14.82% CAGR (2026–2035). Supported by minimally invasive harvesting techniques and higher cell yields per gram of tissue. Adipose-derived stem cells yield 500-fold more mesenchymal progenitors per gram than bone marrow aspirate, and liposuction—the primary collection method—is one of the most commonly performed elective procedures worldwide.

BY INDICATION

Bone & Cartilage Repair: Dominant indication with ~25.7% revenue share in 2025. Aging population and the alternative to total joint replacement drive sustained demand. Bone and cartilage repair indications—particularly knee osteoarthritis—affect over 500 million adults worldwide and represent a USD 7 billion addressable procedure market where MSC cell therapy applications offer a biological alternative to joint replacement.

Cardiovascular Disease: Fastest-growing indication segment at 15.01% CAGR (2026–2035). Reflecting unmet need in chronic heart failure and an expanding Phase III pipeline. Cardiovascular disease remains the leading cause of mortality globally, responsible for approximately 17.9 million deaths annually according to WHO data. These epidemiological tailwinds create sustained demand for regenerative cell transplantation therapies across the forecast period.

BY APPLICATION

Drug Development & Discovery: Dominant application with ~33.8% revenue share in 2025. MSCs as in-vitro screening platforms for multipotent stromal cell research dominate volume, channeling routine preclinical supply. Standardized human MSC lines delivered to pharmaceutical R&D settings anchor this segment.

Disease Modelling: Fastest-growing application segment at 13.6% CAGR (2026–2035). Patient-derived organoid and co-culture systems drive demand as academic centers build specialized cell-processing infrastructure.

BY END USER

Hospitals: Largest segment with ~43.4% share in 2025. Comprehensive oncology and orthopedic service lines and radiopharmaceutical administration requirements dominate volume. Hospitals remain the primary delivery site for regenerative cell transplantation with allogeneic products due to cell-processing infrastructure, specialized cryopreservation, and nuclear pharmacy licensing requirements.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/mesenchymal-stem-cells-market-21855

Regional Outlook

North America — Dominant Market (~43.4% Share, 2025)

The United States generates approximately 82.6% of North American Mesenchymal Stem Cells Market revenue, driven by the NIH HEAL Initiative MSC grants, CMS reimbursement codes for regenerative cell transplantation, and broad funding for multipotent stromal cell research—a single policy ecosystem that converted a laboratory-stage market into one with a structural clinical therapy tail. CMS reimbursement for cell therapies under the hospital outpatient prospective payment system has driven adoption in academic medical centers, while community hospitals increasingly prescribe MSC cell therapy applications to manage chronic disease burden. The US dominates through a combination of high per-patient spending, robust payer coverage, and rapid allogeneic product adoption.

Europe — Second Largest (USD 1.31 Billion, 2025)

Europe’s Mesenchymal Stem Cells Market reflects divergent national strategies—Germany leads regionally with Fraunhofer cell therapy translational programs, contributing 24.3% of regional share, while the UK historically used selective multipotent stromal cell research targeting before broadening coverage through the MHRA Innovative Licensing and Access Pathway at 12.87% CAGR. France contributes ~18.5% of regional share through ANSM adaptive trial frameworks. Italy contributes 10.8% of regional share on San Raffaele Hospital MSC manufacturing unit leadership. Spain is growing at 11.2% CAGR on AEMPS expedited ATMP reviews.

Harmonization pressure from the EU Pharmaceutical Strategy is gradually narrowing these differences, lifting baseline demand across the region. The European Commission’s Pharmaceutical Strategy mandates equitable access to advanced therapy medicinal products, including regenerative cell transplantation across all member states. The Nordic countries hold ~7.4% of regional share on Karolinska-led academic manufacturing consortia at USD 0.09 Billion.

Asia-Pacific — Fastest-Growing Region (15.63% CAGR, 2026–2035)

Asia-Pacific is the engine of the Mesenchymal Stem Cells Market. China holds the largest regional share with ~31.2% of regional revenue, driven by NMPA conditional approval pathway for MSC cell therapy applications—instantly extending regenerative cell transplantation access to the world’s largest patient population. India is growing at 17.54% CAGR on the back of DBT cell therapy manufacturing investment and the INR 1,500 crore National Biopharma Mission. Japan contributes USD 0.18 Billion through PMDA SAKIGAKE designation for multipotent stromal cell research products at steady pace. South Korea is growing at 14.9% CAGR on MFDS regenerative medicine act implementation, with conditional approval of Cartistem for cartilage repair using bone marrow stromal cells continuing to generate real-world evidence.

Middle East & Africa — Emerging Opportunity (5.9% CAGR, 2026–2035)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with Vision 2030 biotech investment arm, contributing ~28.5% of regional share—the sovereign health fund committed USD 450 million to cell and gene therapy infrastructure, positioning the kingdom as a future hub for regenerative cell transplantation in the Gulf region. The UAE is growing at 10.2% CAGR on Dubai Healthcare City regenerative medicine hub development. South Africa contributes USD 0.02 Billion on SAHPRA cell therapy classification framework.

South America — Growing Presence (USD 0.22 Billion, 2025)

Brazil anchors South America’s Mesenchymal Stem Cells Market at ~58.2% of regional revenue, with ANVISA’s updated guidance on advanced therapy products in mid-2024 establishing a clearer pathway for adipose-derived stem cells clinical trials. Access to allogeneic products remains limited by import dependencies, though the Brazilian biotechnology sector has initiated domestic bone marrow stromal cell production feasibility studies. Argentina is growing at 9.3% CAGR on ANMAT regenerative medicine working group expansion.

Competitive Landscape and Recent Developments

The Mesenchymal Stem Cells Market exhibits medium concentration, with the top five companies holding an estimated 32–38% combined revenue share. The Herfindahl-Hirschman Index sits in the 800–1,200 range, reflecting a mix of multinational life-science conglomerates and specialized regenerative medicine developers. Patent expirations and biosimilar entry are gradually fragmenting branded segments, though pipeline innovation in allogeneic platforms sustains competitive moats for first-movers.

The competitive landscape is stratified between allogeneic MSC pioneers serving global regenerative cell transplantation markets, bioprocessing platform expansion specialists capturing CDMO tenders, and consumables suppliers consolidating the multipotent stromal cell research segment.

KEY COMPANIES AND RECENT MILESTONES

Mesoblast Limited (December 2024): Received FDA approval for Ryoncil, the first allogeneic MSC product for pediatric steroid-refractory acute GvHD, marking a watershed moment for the Mesenchymal Stem Cells Market. First-mover in FDA-approved allogeneic MSC cell therapy applications, commanding ~8–11% of global revenue.

Lonza Group (2024–2025): Vertically integrated manufacturing partner with cell therapy CDMO services and bioreactor suites, holding ~6–9% of global revenue. The company benefits from the structural manufacturing tail created by over USD 800 million in combined cell therapy manufacturing suite investments since 2022.

Thermo Fisher Scientific (May 2025): Launched a next-generation xeno-free MSC expansion medium that reduces culture time by 30%, targeting clinical-grade regenerative cell transplantation workflows. Dominant consumables supplier for bone marrow stromal cells culture, holding ~5–8% of global revenue.

Cynata Therapeutics (2024–2025): Scalable induced-pluripotent-derived multipotent stromal cell research platform with CYP-001 iPSC-derived MSC platform, holding ~3–5% of global revenue.

Future Outlook: 2026–2035

By 2030, precision allogeneic MSC theranostics will become the operating system of regenerative medicine. The convergence of companion potency analytics and targeted cell therapy will reshape the Mesenchymal Stem Cells Market through the late 2020s. By 2030, an estimated 40% of newly approved cell therapy manufacturing facilities will incorporate AI-driven potency prediction, creating a diagnostic-manufacturing revenue loop. Machine-learning algorithms trained on thousands of bone marrow stromal cells expansion datasets are expected to predict lot potency with 90%+ accuracy by 2028, reducing release-testing timelines from 14 days to under 72 hours. Start-ups have raised over USD 800 million in venture funding for oncology decision-support tools since 2023.

Allogeneic-driven access expansion and AI-integrated quality control will reframe cost structures by the early 2030s. Patent expirations for key MSC manufacturing processes (expected 2028–2030 in major markets) will trigger platform entry that could reduce regenerative cell transplantation costs by 20–25%. While this compresses per-unit revenue, volume expansion—particularly in Asia-Pacific and South America—is projected to more than offset pricing headwinds.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/stem-cell-therapy-market-6422

https://www.marketresearchfuture.com/reports/regenerative-medicine-market-2220

https://www.marketresearchfuture.com/reports/cell-therapy-market-5066

https://www.marketresearchfuture.com/reports/tissue-engineering-market-2134

https://www.marketresearchfuture.com/reports/induced-pluripotent-stem-cells-market-21852

https://www.marketresearchfuture.com/reports/gene-therapy-market-8399

https://www.marketresearchfuture.com/reports/stem-cell-banking-market-8441

https://www.marketresearchfuture.com/reports/biopharmaceuticals-market-8439

https://www.marketresearchfuture.com/reports/personalized-medicine-market-2937

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery